Options Education · Beginner

Option Buyer vs Option Seller: Who Actually Makes Money in Nifty?

This is the question every new options trader asks. And honestly, it deserves a straight answer instead of the usual "both can be profitable depending on conditions" non-answer. So here it is: Option selling strategies often exhibit higher probability of small gains due to time decay, though they carry tail-risk of large losses. But sellers can blow up their entire account in a single bad session. And buyers, even with the odds against them, make money when they get the timing and environment right. This article breaks down the real difference between the two sides, with actual numbers, so you can decide where you belong.

In This Article

- The Basic Difference Between Buyer and Seller

- The Option Buyer's Reality: Unlimited Upside, Three Enemies

- The Option Seller's Reality: Steady Income, One Catastrophic Risk

- Who Actually Wins? What SEBI Data and Market Structure Tell Us

- Capital Required: How Much You Actually Need for Each Side

- Buyer or Seller: Which One Are You?

The Basic Difference Between Buyer and Seller

Let's get this foundation absolutely right before we go any further, because a lot of confusion starts here.

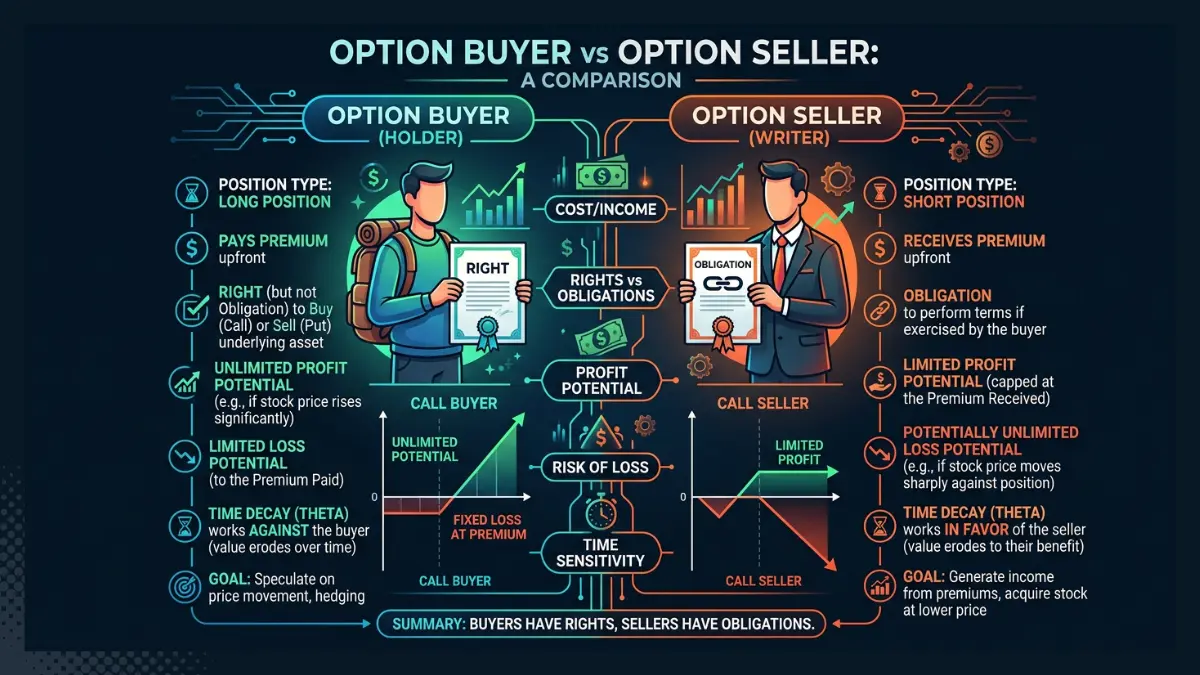

When you buy a Nifty option, you are paying a premium upfront. That premium is your maximum loss. In exchange, you get the right to profit if Nifty moves in your direction. Your upside is theoretically unlimited on calls. Your downside is limited to what you paid. Simple and clean.

When you sell an option, you collect that premium upfront. It lands in your account immediately. But now you have an obligation. If Nifty moves sharply against you, you have to honour that obligation. The maximum profit you can ever make is the premium you collected. The maximum loss is theoretically unlimited on naked positions.

One side pays for optionality. The other side provides it. That is the transaction. Neither is inherently good or bad. They are just fundamentally different risk profiles.

| Feature | Option Buyer | Option Seller |

|---|---|---|

| Upfront cash flow | Pays premium out | Receives premium in |

| Maximum profit | Unlimited (calls) / large (puts) | Capped at premium received |

| Maximum loss | Limited to premium paid | Unlimited (naked) / large |

| Theta (time decay) | Works against you daily | Works in your favour daily |

| Capital needed (1 Nifty lot) | Premium only (~₹5,000–20,000) | Margin of ₹1–1.5 lakh (naked) |

| Margin requirement | None, premium is max loss | High, varies with VIX and strike |

| Probability of small profit | Lower | Higher |

| Probability of large loss | Zero (premium is max loss) | Real and significant |

The Option Buyer's Reality: Unlimited Upside, Three Enemies

Buying options looks like the best deal in trading on paper. You pay a small amount, risk only what you put in, and have theoretically unlimited upside. And yet, 93% of retail F&O traders, almost all of whom buy options at some point, lose money. How?

Three forces work against you the moment you enter a buy position. Miss any one of them and you can lose even when you are right about Nifty's direction.

Enemy 1: Theta decay

Every option loses time value every single day. This is called theta decay. It is not optional. It does not stop on weekends. A weekly Nifty ATM option loses roughly 9% of its premium value per day from theta alone, based on Upstox's analysis of Nifty option chain data. Buy an option for ₹180 on a Wednesday and by the following Monday, if Nifty has not moved at all, your option might be worth ₹90 or less. Nifty does not have to go against you. Time alone can cut your position in half.

Enemy 2: Implied volatility crush

Option premiums have two components: intrinsic value (how much the option is in the money) and time value (which includes implied volatility). Before big events like RBI policy announcements or Budget Day, implied volatility rises as traders buy protection. Premiums inflate. The moment the event is announced and uncertainty resolves, IV collapses. This is called IV crush.

The result: you buy a Nifty put the day before RBI cuts rates by more than expected. Nifty falls 200 points in your direction. You check your option. It has lost value. IV just dropped from 22 to 14 the moment the decision was announced. The volatility premium you paid for was wiped out faster than the delta gain from the 200-point move.

Enemy 3: Wrong strike selection

Far out-of-the-money options are cheap but they carry almost no delta. Delta is the sensitivity of your option to Nifty's movement. A deeply OTM call with Delta 0.05 gains only ₹3.25 for every 100-point Nifty rally (Delta x move x lot size = 0.05 x 100 x 65). Meanwhile, theta is taking ₹8 to ₹12 out of it every day. You need Nifty to move 300 to 400 points just to break even on theta for one week. That happens, but not every week. Buying far OTM options as a routine strategy is paying the market a slow, steady tax.

Feel the Difference Between Buying and Selling. With Zero Real Money.

NiftyWise's free simulator shows you live Greeks on both long and short positions through real historical Nifty scenarios. ₹10 lakh virtual capital. No cost, no risk.

Launch Free Simulator →The Option Seller's Reality: Steady Income, One Catastrophic Risk

Option selling sounds almost too good when you hear it the first time. You collect money upfront. Time works in your favour every single day. You profit if Nifty stays flat, rises slowly, or falls slowly. You do not even need to be right about direction in a range-bound market. You just need to be right that Nifty will not make a dramatic move.

That is a much easier thing to be right about than predicting direction. Most weeks, Nifty does not move dramatically. It chops around, grinds, stays within a range. Sellers collect premium week after week in those environments. It feels almost like rental income.

There is one problem. The weeks when Nifty does move dramatically.

The gap risk that destroys sellers

On 4 March 2026, Nifty fell 685 points in a single session after India reopened post-Holi and absorbed two days of US-Iran war news at once. Option sellers who had written naked puts the Friday before watched their positions move from small profit to massive loss in a single morning. The premium they had collected over several weeks evaporated in hours.

This is the defining characteristic of selling. The income is slow and steady. The losses are sudden and large. You spend weeks building up ₹30,000 in collected premium. One circuit-breaker day wipes out ₹1.5 lakh. Your five-week streak is erased with interest.

What selling actually requires

First, capital. Under SEBI's 2025 margin rules, selling a single naked Nifty lot requires ₹1 lakh to ₹1.5 lakh in upfront margin, depending on the strike, VIX level, and whether it is a naked or hedged position. The margin fluctuates daily as VIX changes. In the current high-VIX environment of March 2026, margins are on the higher end of that range. You need significantly more capital to be a seller than a buyer.

Second, emotional discipline. Holding a short option position when Nifty is moving sharply against you is psychologically brutal. The urge to exit at a large loss rather than hold is overwhelming. Sellers who do not have clear rules for when to cut losses tend to hold too long, turning a bad loss into a catastrophic one.

"Option selling is like collecting rent from a property. Most months are fine. But once in a while, there is a flood. The people who survive long-term are the ones who bought insurance for the flood before it happened, not after."

How professional sellers manage this

Professional option sellers almost never sell naked. They use defined-risk structures: spread positions, Iron Condors, strangles with hedges. Under SEBI's current margin rules, hedged positions benefit from significantly lower margin requirements. A naked short Nifty call might need ₹1 lakh in margin. The same call combined with a long call 300 points higher (a spread) might need only ₹30,000 to ₹40,000, because the exchange recognises the capped risk and reduces the SPAN margin accordingly.

Who Actually Wins? What SEBI Data and Market Structure Tell Us

Let's look at the actual numbers from SEBI's September 2024 study, which covered FY22 to FY24 and analysed data from over 1.13 crore individual traders.

Individual retail traders as a group: 93% lost money. Average loss per person over three years: ₹2 lakh. The top 3.5% of loss-makers, around 4 lakh traders, lost an average of ₹28 lakh each over the period.

But here is where it gets interesting. Who made money?

Proprietary traders (essentially professional selling desks) earned ₹33,000 crore in gross trading profits in FY24 alone. Foreign Portfolio Investors earned ₹28,000 crore in the same year. SEBI specifically noted that 96% of proprietary trader profits and 97% of FPI profits came from algorithmic trading. Most of that algorithmic activity involves systematically selling options and collecting premium with risk controls that retail traders cannot replicate manually.

Does this mean all retail sellers win?

No. And this is a crucial nuance. SEBI's data shows that 93% of individual F&O traders, which includes both buyers and sellers, lost money. Many retail sellers also lose because they sell naked without proper hedges, get caught in gap moves, and do not use systematic rules. The edge in selling comes from discipline, capitalisation, and hedging. Not just from being on the selling side.

The individual retail sellers who consistently profit tend to do one or more of the following: use defined-risk spread structures that cap their downside, size positions conservatively relative to their capital, exit when positions hit a pre-defined loss limit regardless of their view, and stay out of positions when India VIX is spiking violently.

Capital Required: How Much You Actually Need for Each Side

This is a practical section because the capital difference between buying and selling is massive and most beginners do not realise it upfront.

| Trade type | Capital needed (approx.) | Max loss | Based on |

|---|---|---|---|

| Buy 1 lot Nifty ATM call | ~₹11,700 | ₹11,700 (premium paid) | ~₹180 premium x 65 lot size |

| Buy 1 lot Nifty ATM put | ~₹11,050 | ₹11,050 (premium paid) | ~₹170 premium x 65 lot size |

| Sell 1 lot Nifty OTM call (naked) | ₹1–1.5 lakh | Theoretically unlimited | SEBI 2025 margin rules |

| Sell 1 lot Nifty OTM put (naked) | ₹1–1.5 lakh | Theoretically unlimited | SEBI 2025 margin rules |

| Bull call spread (buy ATM, sell OTM) | ~₹4,550 | Net debit only | Net premium x 65 |

| Iron Condor (4 legs, hedged) | ~₹30,000–50,000 | Capped at spread width | Reduced SPAN due to hedged risk |

Premium figures above are approximate for illustrative purposes and vary with market conditions, VIX level, and time to expiry. Always verify current margins with your broker before trading.

The practical implication: if you have ₹50,000 in your trading account, option buying is genuinely accessible. You can buy one or two lots with limited downside. Option selling at scale is not realistic at that capital level, because one lot of naked selling ties up your entire account in margin and leaves no room for adverse moves.

With ₹3 lakh or more, selling becomes practical. Most experienced retail sellers recommend keeping capital well above minimum margin requirements, so that a large adverse move does not trigger a forced square-off before they can manage the position.

Buyer or Seller: Which One Are You?

This is not about which side is better in the abstract. It is about which one fits your capital, personality, and current skill level.

- You have less than ₹1.5 lakh available for trading

- You are still learning how options work

- You cannot monitor positions closely during market hours

- You want defined, known maximum loss on every trade

- You have a strong view on a specific near-term event

- You have ₹3 lakh or more dedicated to options trading

- You understand Greeks and can track delta exposure daily

- You can monitor positions during market hours

- You have clear rules for cutting losses before they get large

- You use defined-risk structures, not naked positions

The most common progression I have seen works like this. Start as a buyer to learn how options behave. Understand theta, IV, and strike selection through real experience. After 3 to 6 months of consistent practice, move into defined-risk selling structures like credit spreads and Iron Condors. That transition from buyer to structured seller is where most serious retail traders end up.

The simulator is the best place to work through both sides. Buy a straddle through a Budget Day scenario and watch IV crush. Sell a strangle through a geopolitical shock scenario and watch gap risk play out. Do that enough times with virtual money and your intuition about both sides becomes something you cannot get from reading alone.

🎯 Option buyer vs option seller: the short version

- Buyers pay premium upfront and have limited loss but unlimited upside. Sellers collect premium and have capped profit but large or unlimited loss on naked positions.

- Theta works against buyers every single day. It works in favour of sellers. This is the fundamental structural advantage of selling.

- SEBI's 2024 study: proprietary traders earned ₹33,000 crore in FY24 profits, with 96% coming from algorithmic trading. Most of that is systematic selling. Individual retail traders collectively lost over ₹61,000 crore.

- Under SEBI's 2025 margin rules, selling one lot of naked Nifty options requires ₹1 lakh to ₹1.5 lakh in upfront margin. Buying one lot costs only the premium, typically ₹5,000 to ₹20,000. The capital barrier to selling is very high.

- Nifty's lot size is now 65, revised from January 2026. All premium calculations and margin estimates should use 65, not the old 75.

- A commonly observed progression among retail participants is start buying to understand behaviour, then transition to defined-risk selling structures like spreads and Iron Condors once you have consistent experience.

- Neither side makes money automatically. 93% of retail F&O traders, including both buyers and sellers, lost money between FY22 and FY24. The edge comes from discipline and structure, not from simply choosing one side over the other.

Frequently Asked Questions

Is option selling always better than buying in India?

No. Selling has a statistical edge in calm, range-bound markets where implied volatility is elevated. Buying has an edge when VIX is unusually low and a clear catalyst is approaching. Right now in March 2026, with VIX around 22 and a major geopolitical event in play, both sides face challenges. Sellers face severe gap risk from the Iran war. Buyers face expensive premiums and the risk of IV crush when the war eventually resolves. The right approach depends on reading the current environment, not on picking a side and sticking to it dogmatically.

How much money do I need to start selling Nifty options?

To sell a single naked Nifty lot, you need ₹1 lakh to ₹1.5 lakh in margin under SEBI's current rules. But that is the absolute minimum for one lot. In practice, keeping your entire capital tied up in margin for one naked position leaves no room to manage the position if it moves against you. Most experienced sellers recommend keeping total capital at three to five times the minimum margin requirement. For a single-lot seller, that means ₹3 lakh to ₹5 lakh dedicated to the position. Spread positions (hedged selling) require significantly less margin due to the capped risk structure.

Can a beginner start with option selling in India?

Technically yes, but it is not advisable. Selling requires understanding of Greeks, particularly Delta and Vega, to manage positions as the market moves. It requires the discipline to cut losses at a pre-defined level rather than holding and hoping. And it requires enough capital to absorb adverse moves without a forced square-off. These are skills that take time to build. Starting with defined-risk buying strategies, learning how options behave, and only moving to selling after 3 to 6 months of consistent practice and study is the more sensible path for most beginners.

What changed for option sellers after SEBI's 2024 and 2025 rules?

Several things changed that directly affect sellers. Full premium collection is now required upfront from buyers, which reduces some of the leverage available to buyers. Peak margin rules require sellers to maintain full margin throughout the trading day, not just at end of day. Calendar spread margin benefits were removed on expiry days, increasing the cost of holding these positions through expiry. And lot sizes changed from January 2026, with Nifty moving from 75 to 65. The net effect: selling is more capital-intensive than it was before 2024, and the old intraday leverage that some sellers relied on is no longer available.

What is the Nifty lot size in 2026?

The Nifty 50 lot size is 65 units per contract, effective from January 2026, revised from the previous 75. This change was mandated by NSE via circular and applies to all weekly, monthly, and longer-tenure contracts expiring from January 2026 onwards. When calculating the rupee value of any premium, margin, or P&L on Nifty options, always multiply by 65. Using the old lot size of 75 will give you incorrect numbers.

Practice Both Sides of Nifty Options Before You Risk Real Capital

NiftyWise's free simulator lets you trade as buyer or seller through real historical Nifty scenarios. Watch theta, Delta, and VIX behave in real time. ₹10 lakh virtual capital. Free forever.

Launch Free Simulator →⚠️ Disclaimer: Please Read. This article represents the personal opinions and analysis of the NiftyWise editorial team.. It is for educational purposes only and does not constitute investment advice, a trading recommendation, or financial guidance of any kind. The reviewer has no financial interest in the platform mentioned. Reviewed from a financial literacy and compliance perspective .No endorsement of any platform is intended. All premium, margin, and capital figures are approximate and for illustration purposes only. Actual margins vary daily based on VIX, strike selection, and SEBI/NSE rules and are subject to change. Nifty lot size of 65 is based on NSE circular effective January 2026. Always verify current lot sizes and margin requirements with NSE or your broker before trading. SEBI profit and loss data referenced is from SEBI's updated study published September 2024 covering FY22 to FY24. NiftyWise is not registered with SEBI as an Investment Adviser, Research Analyst, or Stockbroker. Past performance, simulated or actual, is not indicative of future results. Options trading carries substantial risk of loss. As per SEBI's updated study (September 2024): 93% of individual traders in the equity F&O segment incurred losses between FY22 and FY24, with aggregate losses exceeding ₹1.8 lakh crore. Please consult a SEBI-registered Investment Adviser before making any investment decisions. Visit sebi.gov.in for a list of registered advisers.